The tres amigos of Advanced TV

When I started in media in 2004, the world of video was very different than what it is today. The concept of online video was basically limited to funny video material such as bad day, numa numa and peanut butter jelly time shared via work emails. Television was the only audio visual medium available for advertising purposes. In just 15 years the landscape has changed tremendously. Television is still around, but the video opportunities for advertiser have multiplied with the advent of the internet. In particular, the media channels included in Advanced TV represent perhaps the most important evolution of digital video placements since the pre-roll.

The IAB defines Advanced TV as any television content or advertising that has evolved beyond traditional, linear television delivery models. Connected TV, Addressable TV and Programmatic Linear TV are all media included in this definition. Occasionally digital video, such as pre-roll and mid-roll are also included but today we will concentrate on the 3 mentioned above. Consumer adoption of Advanced TV technologies is growing year over year and these platforms are expected to achieve two-digit growth in advertising investment in next years to come with Pharma, Travel and CPG driving investment on this medium. Today, we’ll provide an introduction to each of the Tres Amigos of Advanced TV : connected TV, addressable TV and “programmatic” TV.

Courtesy: U.S TV $ Video Market at-a-glance-Q3 2017 – Videology

Connected TV

Connected TV is television that is connected to the open internet either through the cable provider set top box or through a consumer electronic device like a streaming box or game console, also known as OTT or over the top box. It is currently estimated that 64% of U.S residents own a CTV device with an annual growth rate of about 10% until 2021. Connected TV offers the ability to target audiences layering 1st and 3rd party data, using retargeting, look-alike and cross device targeting tactics and getting as granular as DMA level. In terms of measurement, video completion rates, GRPs or conversions are all typically KPIs used in a connected TV campaign, depending of the strategy this medium is part of – Nielsen OTT and Nielsen DAR allow marketers to measure connected tv impact through traditional metrics such as GRPs-.

Among the advantages of the platform we have the non-skippable feature of its inventory, the 100% viewability rates and the high completion rates, around 95%. Although currently the total inventory of OTT represents only a fraction of linear TV, it is growing rapidly, driven by a higher demand which translates into higher viewership, the increasing availability of content, providers as well as the amount of ad time allocated by OTT operators. Examples of providers include Roku, Hulu, Sling TV, CBS All Access, HBO Now, Amazon Prime Video, Netflix, Sony Playstation Vue etc.

Courtesy: Comscore 2016

Addressable TV

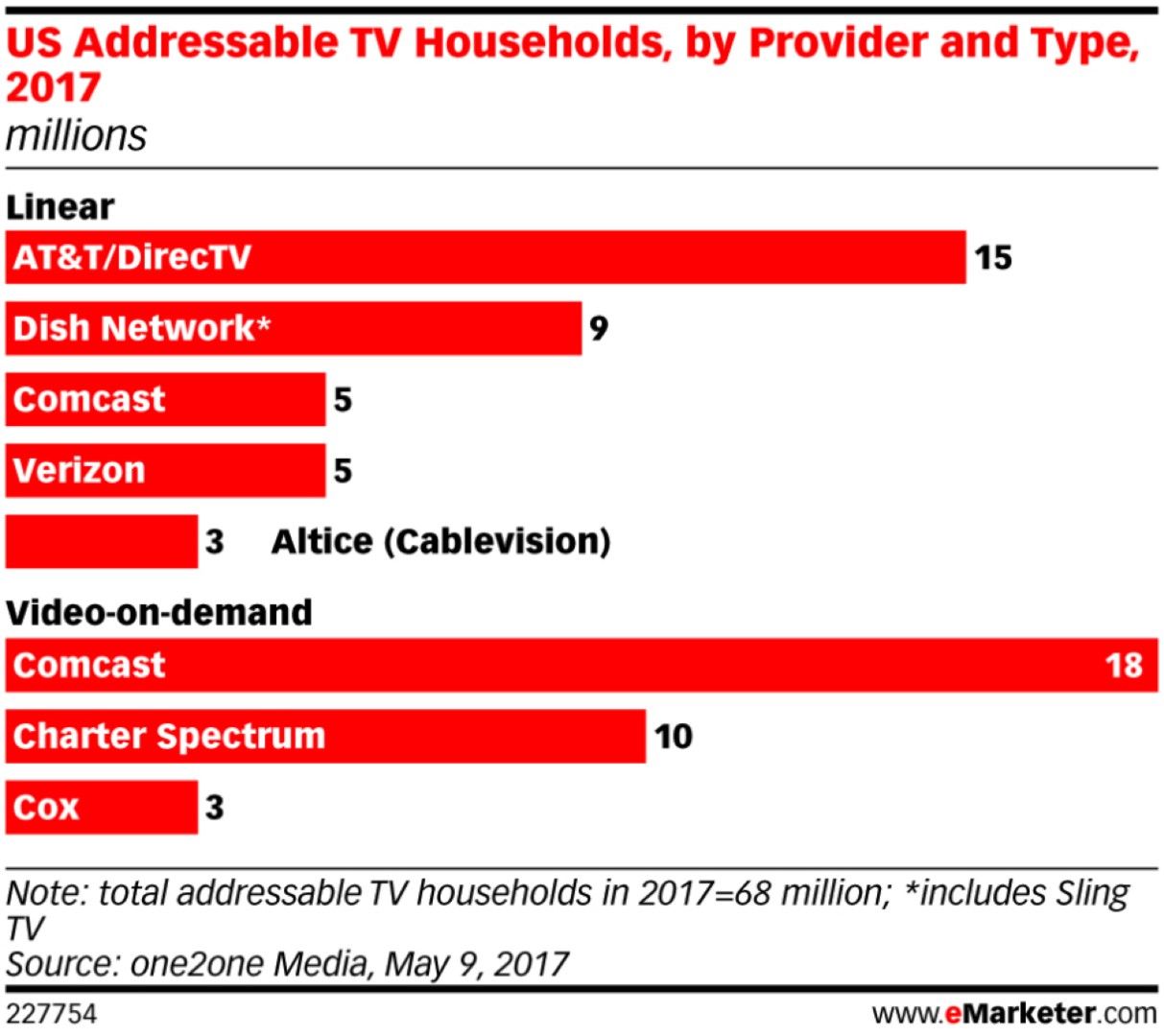

What we know as addressable TV refers to any technology that lets you show different ads to different audience segments watching the same TV program on IPTV and set top boxes. These segments could be defined by behavioral, demographic and geographic factors from 1st, 2nd or 3rd party data sets. Among the advantages of this type of advanced TV we have the superior ROI and the potential for an expansion of both available addressable inventory and the number of households that can be reached. Additionally, marketers can leverage 1st and 3rd party data going as granular as the household level. Currently, most advertisers use addressable TV as a complement to national TV plans as buyers can only work with the subset of homes that are addressable-enabled. It is estimated that 68MM of households in the U.S have the ability to be targeted with addressable TV but only 37MM are fully enabled. The inventory is provided by companies such as Dish Network, AT&T, Direct TV, Comcast and Cablevision/ Altice.

Courtesy: e-Marketer 2018

Programmatic Linear TV (PTV)

Defined as the use of software platform to automate the buying or selling of live TV advertising distributed through cable, satellite or broadcast networks. The promise of programmatic linear TV is enticing to media buyers and marketers alike: the idea of being able to buy linear television inventory through your DSP with a bidding system that would allow the digital trader to pay fair market prices based on demand for those precious 30s spots during prime time and with the ability of optimizing spots and budgets based on performance throughout the length of a media flight; but the reality is that fully automated transactions are not yet available as purchase orders and execution systems are not quite integrated with the various programmatic planning tools. PTV is available in approximately 90MM households, but networks and stations often hold back inventory to be sold traditionally (IO Based) at higher prices. Spending in “programmatic” TV, or the hybrid of programmatic/traditional version currently available, is estimated in $1.13 billion in 2017 and projected to $3.8billion in 2019, representing approximately 5% of the total U.S TV spend at that point. Among the advantages of PTV is the ability to reach audiences via 1st and 3rd party data, by genre or category, by day part and day of week and in terms of geography it can go as granular as DMA. Some providers include Wideorbit, Clypd, AdMore, Audience Express, Placemedia, Cadent among others.

Parting Thoughts

The future for advanced TV is bright. Inventory for all of its platforms will only grow year after year, increasing the scalability of the video channels. Audience targeting accuracy will only get better as new algorithms are developed, overall providing with a solid alternative – or ultimately, a replacement- to linear TV. But its growth won’t be as fast as it could be as there is external pressure to slow it down as much as possible. Yes, the number of cable cutters is increasing exponentially among the younger generations and OTT devices are near-ubiquitous, but the 50+ crowd still love their prime time fix, old habits are hard to break, and these folks keep generating revenue to the networks. Additionally, and perhaps most importantly, traditional TV also represents a considerably larger source of commission for traditional advertising agencies, who at the end of the day are responsible for the allocation of advertisings dollars. Independently of the external forces trying to undermine the proliferation of advanced TV, it seems pretty clear to all of us in the industry that there is no turning back. Traditional ways of video content consumption are shifting to digital and traditional television will have to adapt, if they want to continue being a player in the game.

Sources: IAB, The Trade Desk, eMarketer, Forrester, TubeMogul